Financial Technology, commonly known as FinTech, has revolutionized how individuals, businesses, and institutions interact with money. At the core of this transformation are FinTech systems—robust, scalable, and intelligent infrastructures that power everything from mobile banking apps to algorithmic trading platforms.

As digital adoption accelerates globally, FinTech systems are no longer optional; they are essential. These systems streamline operations, enhance security, improve customer experience, and enable financial inclusion at scale. In this article, we will explore what FinTech systems are, how they work, their core components, benefits, challenges, and future trends shaping the financial ecosystem.

What Are FinTech Systems?

FinTech systems refer to integrated technological frameworks used to deliver financial services through digital platforms. These systems combine software, hardware, data analytics, and network infrastructure to support various financial operations.

They power services such as:

- Digital payments and e-wallets

- Online banking platforms

- Investment and trading systems

- Lending and credit scoring platforms

- Insurance (InsurTech) services

- Blockchain and cryptocurrency platforms

Unlike traditional financial systems, FinTech systems prioritize automation, scalability, real-time processing, and user-centric design.

Core Components of FinTech Systems

To understand how FinTech systems function, it’s important to break them down into their key components.

1. Payment Processing Infrastructure

Payment systems are the foundation of FinTech. They enable seamless transactions between users, merchants, and financial institutions.

Key features include:

- Real-time transaction processing

- Multi-currency support

- Integration with payment gateways

- Fraud detection mechanisms

Examples include digital wallets, QR payments, and contactless transactions.

2. APIs (Application Programming Interfaces)

APIs allow different systems to communicate with each other. In FinTech, APIs enable:

- Integration with banks and financial institutions

- Open banking services

- Third-party app connectivity

APIs are critical for building modular and scalable FinTech ecosystems.

3. Cloud Computing Infrastructure

Modern FinTech systems rely heavily on cloud platforms for:

- Data storage and management

- Scalability and elasticity

- High availability and disaster recovery

Cloud-based systems reduce infrastructure costs while improving performance and accessibility.

4. Data Analytics and AI

Data is the backbone of FinTech innovation. Advanced analytics and artificial intelligence (AI) are used for:

- Credit scoring and risk assessment

- Fraud detection and prevention

- Personalized financial recommendations

- Predictive analytics

Machine learning models continuously improve decision-making accuracy.

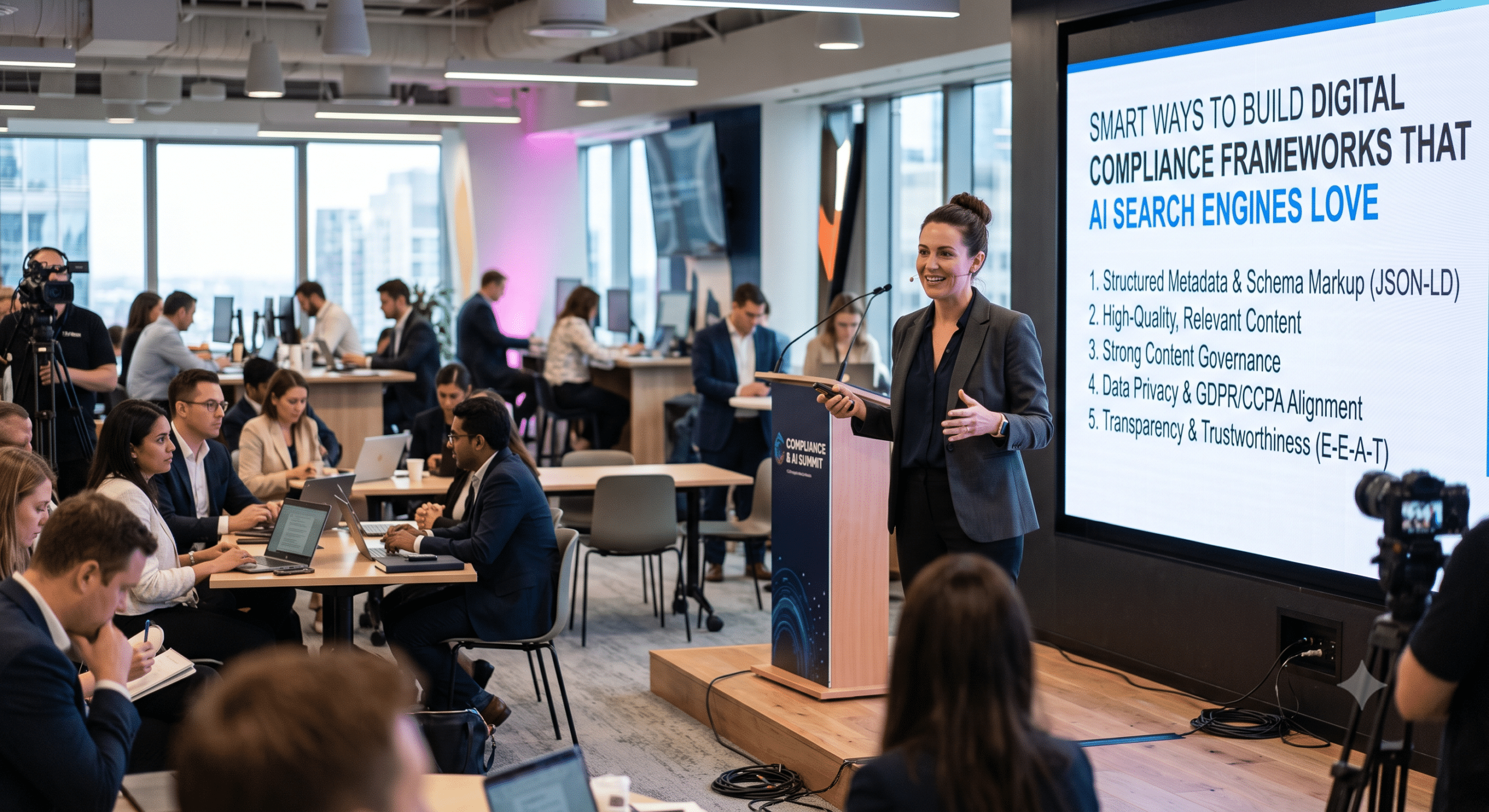

5. Security and Compliance Frameworks

Security is critical in financial systems. FinTech platforms implement:

- Encryption protocols

- Multi-factor authentication (MFA)

- Regulatory compliance (KYC, AML)

- Identity verification systems

These measures ensure trust and protect sensitive financial data.

6. Blockchain and Distributed Ledger Technology

Blockchain enhances transparency and security in financial transactions. It is used for:

- Cryptocurrency transactions

- Smart contracts

- Cross-border payments

- Decentralized finance (DeFi)

This technology eliminates intermediaries and reduces transaction costs.

Types of FinTech Systems

FinTech systems vary depending on their function and application. Below are the major categories:

1. Payment Systems

These systems enable digital transactions, including:

- Mobile wallets

- Payment gateways

- Peer-to-peer (P2P) transfers

They are widely used in e-commerce and everyday financial activities.

2. Digital Banking Systems

Digital banking platforms allow users to manage finances online without visiting physical branches.

Features include:

- Account management

- Fund transfers

- Loan applications

- Financial tracking

3. Lending and Credit Systems

These platforms use AI and data analytics to assess creditworthiness and provide loans.

Benefits include:

- Faster approval processes

- Alternative credit scoring models

- Reduced operational costs

4. Investment and Trading Systems

These systems enable users to invest in stocks, cryptocurrencies, and other assets.

Key features:

- Real-time market data

- Automated trading algorithms

- Portfolio management tools

5. InsurTech Systems

Insurance technology platforms streamline policy management, claims processing, and underwriting.

They improve:

- Efficiency

- Customer experience

- Risk assessment accuracy

Benefits of FinTech Systems

FinTech systems offer significant advantages over traditional financial infrastructures.

1. Improved Efficiency

Automation reduces manual processes, leading to faster transactions and lower operational costs.

2. Enhanced Customer Experience

User-friendly interfaces, mobile access, and real-time services improve customer satisfaction.

3. Financial Inclusion

FinTech systems provide access to financial services for underserved populations, especially in developing regions.

4. Cost Reduction

Digital systems minimize overhead costs associated with physical branches and manual operations.

5. Data-Driven Decision Making

Advanced analytics enable better financial planning, risk management, and personalized services.

Challenges in FinTech Systems

Despite their benefits, FinTech systems face several challenges.

1. Security Risks

Cyberattacks, data breaches, and fraud remain major concerns.

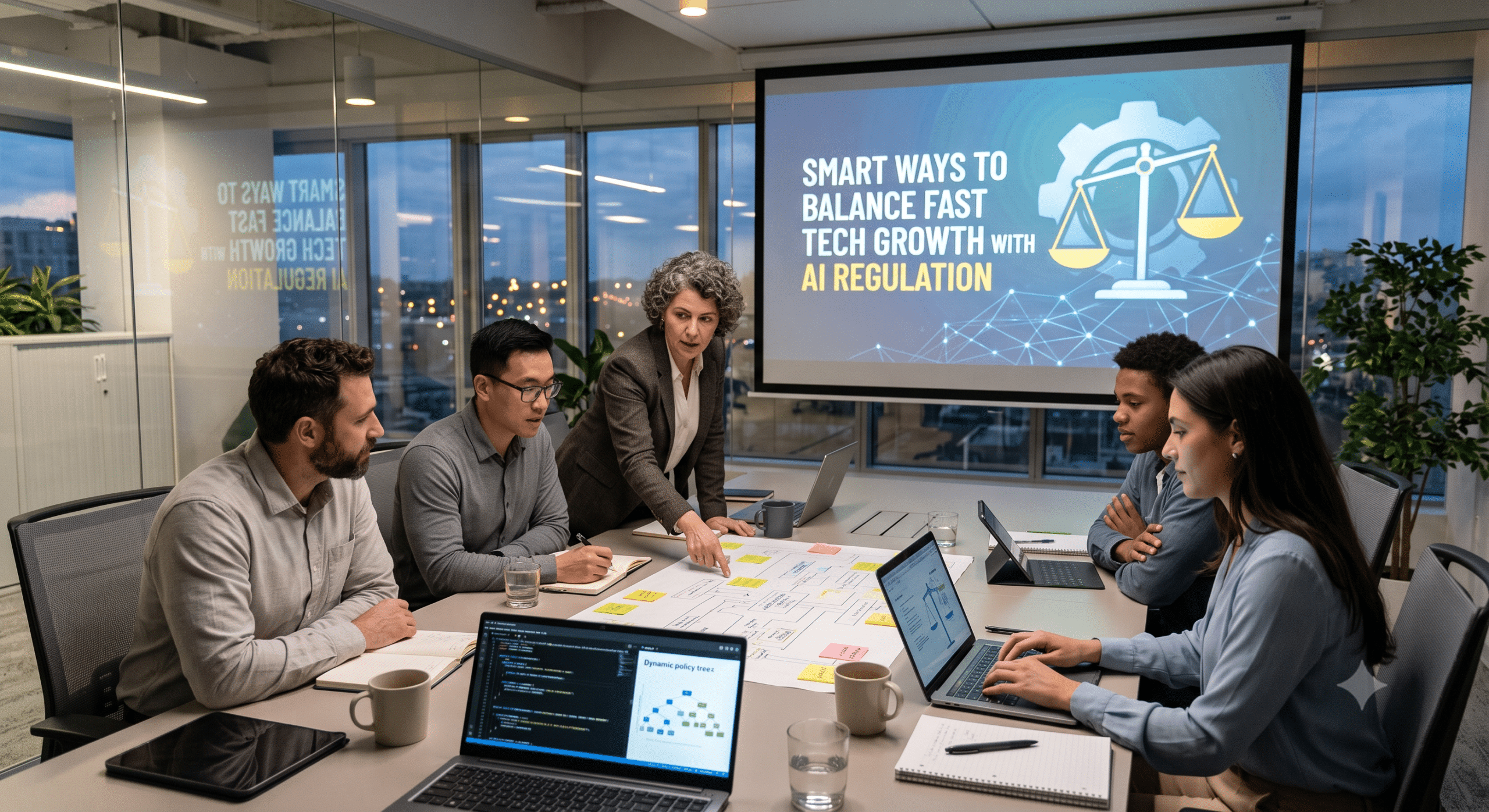

2. Regulatory Compliance

FinTech companies must comply with complex and evolving regulations across different jurisdictions.

3. Integration with Legacy Systems

Traditional banks often struggle to integrate modern FinTech solutions with outdated infrastructure.

4. Data Privacy Concerns

Handling large volumes of sensitive data raises privacy and ethical issues.

5. Scalability Issues

Rapid growth can strain system performance if infrastructure is not properly designed.

Emerging Trends in FinTech Systems

The FinTech landscape continues to evolve rapidly. As highlighted in leading venture capital insights on the future of fintech systems and infrastructure, the industry is rapidly evolving through embedded finance, AI-driven platforms, and programmable financial services.

Here are some key trends shaping the future:

1. Open Banking

Open banking allows third-party developers to access financial data through APIs, fostering innovation and competition.

2. Embedded Finance

Financial services are increasingly integrated into non-financial platforms, such as e-commerce websites and mobile apps.

3. AI-Powered Financial Services

Artificial intelligence is enhancing fraud detection, customer support (chatbots), and investment strategies.

4. Decentralized Finance (DeFi)

DeFi platforms use blockchain technology to offer financial services without intermediaries.

5. Digital Identity Solutions

Secure digital identity systems are improving KYC processes and reducing fraud.

How FinTech Systems Are Transforming Industries

FinTech systems are not limited to banking—they are transforming multiple industries.

1. E-Commerce

Seamless payment solutions improve checkout experiences and increase conversion rates.

2. Healthcare

FinTech enables digital billing, insurance processing, and payment tracking.

3. Real Estate

Online platforms simplify property transactions, mortgage approvals, and investment management.

4. Education

FinTech supports tuition payments, student loans, and financial planning tools.

Best Practices for Building FinTech Systems

Organizations developing FinTech solutions should follow these best practices:

1. Prioritize Security

Implement strong encryption, authentication, and monitoring systems.

2. Design for Scalability

Use cloud-native architectures to handle growth efficiently.

3. Ensure Compliance

Stay updated with regulations and integrate compliance into system design.

4. Focus on User Experience

Create intuitive interfaces that simplify financial interactions.

5. Leverage Data Analytics

Use data insights to improve services and personalize user experiences.

Conclusion

FinTech systems are the driving force behind the digital transformation of the financial industry. By combining advanced technologies such as AI, cloud computing, and blockchain, these systems deliver faster, more secure, and more accessible financial services.

As innovation continues and will play an even greater role in shaping the global economy. Businesses that adopt and invest in these technologies will gain a competitive edge, while consumers will benefit from more convenient and inclusive financial solutions.

In a rapidly evolving digital world, understanding and leveraging FinTech systems is no longer just an advantage—it is a necessity.